By Neno Duplan, CEO, Locus Technologies

Reading Time: 9 minutes 50 seconds

Audits used to be episodic events: an annual compliance review, a periodic regulator inspection, or a certification renewal. Today, audits are becoming a continuous operating condition. The “audit” might still be a formal visit from a regulator, but it could just as easily be a limited-assurance engagement on ESG or SB253 disclosures, a customer-led supplier assessment, an insurer’s risk review, or an internal investigation triggered by an incident or whistleblower report.

What’s changed isn’t only the frequency. It’s the expectation of proof.

Organizations are increasingly asked not just “What did you report?” but “Show me exactly how you derived it, end to end, down to the source record, the calculation logic, the approver, and the evidence that it was controlled.” That expectation is what turns ordinary data management into something more demanding: audit-ready lineage.

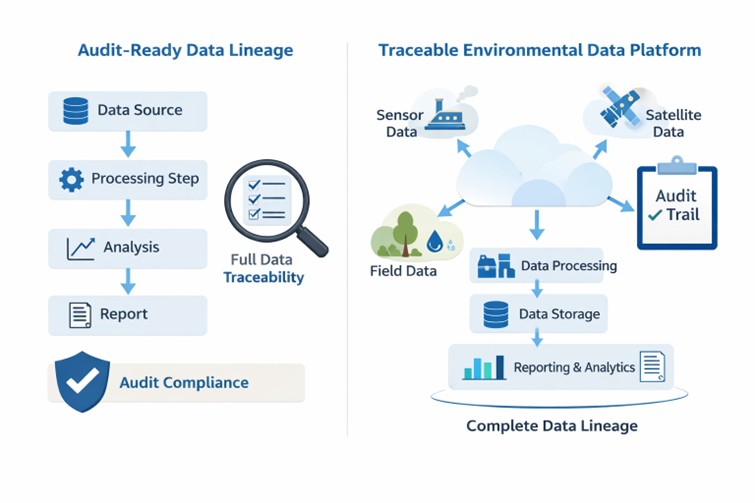

Audit-ready lineage means you can trace each reported value, such as emissions total, wastewater discharge reading, safety rate, spill count, permit deviation, or water withdrawal volume, back to its origin with a defensible chain of custody. A best-effort reconstruction in spreadsheets won’t suffice. A shared drive full of PDFs and email trails won’t cut it. It demands a system of record that preserves the “who/what/when/why” of data, calculations, and decisions, and can reproduce the result under scrutiny.

This is where many well-intentioned environmental and sustainability programs struggle. Not because teams don’t care, but because their technology stack was built for reporting, not for proof. And the difference between reporting and proof is exactly where risk lives.

The audits your organization is likely to face

In most industrial, manufacturing, energy, and resource-intensive sectors, the audit landscape is broad and widening. A unified platform is no longer a “nice to have” because these audit types overlap in data, stakeholders, and timing:

Regulatory compliance audits and inspections. These include environmental compliance (air, GHG, clean fuels carbon intensity, waste, water, stormwater, chemical management), permit adherence, monitoring and sampling records, and documentation of corrective actions. The focus is often on whether required monitoring occurred, whether values exceeded thresholds, and whether deviations were documented and addressed.

Operational and management system audits. ISO-style audits (environmental, health, and safety), internal EHS program audits, and enterprise risk audits often assess whether processes are standardized, controlled, and repeatable across sites.

Safety and incident investigations. Safety audits can begin as routine checks and quickly become formal inquiries after a recordable injury, a near-miss trend, a contractor incident, or a serious event. These audits probe timeliness, completeness, approvals, and whether actions were taken and verified.

Third-party assurance of ESG and sustainability disclosures. As sustainability reporting matures, it increasingly attracts third-party review. These engagements often focus on the quality of the underlying data and controls, including boundaries, completeness, calculation methods, change management, and documentation.

Customer and supply chain assessments. Large customers may require evidence of environmental and safety performance, water stewardship practices, and governance. These assessments can function like audits, with requests for source evidence and process documentation.

Financial, insurance, and transaction diligence. Lending terms, insurance underwriting, and M&A diligence commonly require EHS and environmental liability assessments, as well as evidence that reported performance metrics are reliable. SOC-style audits are part of this.

The common thread: regardless of the “audit label,” the work is fundamentally the same. You need to gather data from many systems and sites, apply consistent rules, preserve evidence, and demonstrate control.

What’s at stake: penalties, operational disruption, and credibility loss.

Organizations often treat audits as a compliance cost. That’s understandable, but incomplete. The real stakes sit in three categories:

- Direct consequences: fines, penalties, legal exposure. In regulatory contexts, inaccurate, missing, or late reporting can trigger monetary penalties, mandatory corrective actions, and heightened oversight. In safety contexts, deficiencies can escalate to enforcement actions, litigation, or mandated program changes.

- Operational consequences: downtime, delays, and resource drain. Audits consume time from plant teams, EHS staff, legal, operations, and executives. When data is fragmented, the audit response becomes a fire drill—pulling records from email, spreadsheets, local databases, and legacy systems. That’s not just inefficient; it can interrupt operations and delay strategic work.

- Strategic consequences: trust, capital, and reputation. ESG disclosures and sustainability claims increasingly influence customer decisions, investor confidence, access to capital, insurance terms, and brand credibility. If your organization cannot substantiate reported metrics (or must restate them) credibility damage can be far more costly than any single fine.

Audit readiness is no longer just risk avoidance. It’s a capability that protects operational continuity and supports strategic credibility.

Why confidence breaks down when audits happen

Most organizations don’t fail audits because they lack data. They fail because they can’t prove the integrity of data across a complex reality with multiple sites, heterogeneous systems, changing requirements, and human workflows.

Common obstacles include:

Fragmentation across point solutions. Many companies run separate tools for EHS compliance, safety, ESG reporting, and water management. Each system might do its job, but they don’t share a consistent data model, governance layer, or evidence approach. The result is “multiple versions of truth,” especially when the same concepts appear in different places (facilities, organizational boundaries, emission factors, incident definitions, water sources, discharge points).

Spreadsheet-driven consolidation. Spreadsheets are powerful but brittle in audit contexts. They hide transformation steps, encourage local variations, and make it difficult to preserve a defensible audit trail of changes, approvals, and calculation logic over time.

Unclear ownership and inconsistent workflows. Data confidence collapses when it isn’t clear who owns each metric, who approves it, what constitutes acceptable evidence, and how exceptions are managed.

Changing definitions and boundaries. ESG and environmental reporting often depend on boundaries and methods such as organizational control models, facility lists, emission factors, materiality thresholds, and data completeness rules. If those change (and they will) you need versioned governance, not informal “tribal knowledge.”

Evidence that exists but isn’t connected. Many organizations have the documents: permits, lab results, calibration records, invoices, manifests, and corrective action logs. But they’re stored separately from the reported metrics. Auditors don’t just want to know the document exists; they want it tied to the exact reported value and period.

These issues are not primarily “people problems.” They are system problems. They arise when the environmental data platform cannot provide lineage as a first-class function.

The interconnectedness of audit-relevant information

One reason audit readiness is so hard is that EHS, ESG, safety, and water are not separate realities. They share data, often in ways that aren’t obvious until an audit forces you to reconcile them.

A few examples:

Facility and organizational structures. The same facility list drives air emissions reporting, waste tracking, water withdrawals, safety incident rates, and ESG rollups. If each system maintains its own version, reconciliation becomes an audit hazard.

Operational activity data. Production volumes, operating hours, fuel usage, purchased utilities, and equipment inventories are often inputs to multiple metrics. These inputs may come from ERP, MES, utility portals, and site logs—systems not designed for audit-ready environmental lineage.

Events and corrective actions. A spill might be both an environmental compliance event and an ESG disclosure consideration, with associated safety implications. Corrective actions may span multiple departments, and auditors may test whether actions were tracked to closure and verified.

Water management as a cross-cutting domain. Water withdrawals, discharges, sampling, and stormwater compliance can intersect with community commitments, risk assessments, and ESG narratives. The same discharge monitoring result may appear in compliance reporting and sustainability performance indicators.

In other words, the problem isn’t just data collection. It’s the “connective tissue” between domains, so that a reported ESG number can be traced to operational and compliance realities, with consistent definitions and evidence.

The technical challenges of responding to an audit

When audit requests arrive, organizations face a predictable sequence of technical hurdles:

Data acquisition from multiple sources. Environmental data lives in many places such as instrument systems, lab systems, contractor reports, utility portals, ERP, legacy databases, and site-level tools. Without robust integration and a structured ingestion approach, teams resort to manual extracts and one-off transformations.

Normalization and unit consistency. Auditors often test whether values were transformed correctly (units, time periods, boundaries, emission factors, rounding). If transformations happen in spreadsheets or ad hoc scripts, reproducibility becomes fragile.

Calculation transparency. If the system can’t show the calculation method, inputs, and parameter values used at the time of reporting, you cannot defend the output. “We usually calculate it this way” is not audit-grade.

Change control and versioning. Metrics evolve. Factors update. Boundaries shift. Without explicit versioning, you risk retroactively changing historical results or losing the ability to reproduce what was reported last quarter.

Workflow traceability. Who entered the data? Who reviewed it? What exceptions were flagged? What was overridden, and why? Audit-ready lineage requires workflow metadata as part of the record, not a separate email chain.

Evidence linkage. Documents and records must be attached directly to the metric, time period, facility, and workflow step they support. Otherwise, evidence becomes a scavenger hunt.

Security and access controls. Audits often require read-only access, role-based segregation of duties, and demonstrable control over who can edit what. Security isn’t separate from lineage—it’s part of proving integrity.

These are platform-level problems. They can’t be solved reliably with disconnected applications, bolt-on integrations, or spreadsheet-based rollups.

How strategic technology choices resolve this and why

The strategic shift is to treat environmental and sustainability data like financial data: governed, controlled, traceable, and reproducible. That requires a unified platform approach; one designed for audit-ready lineage across EHS, ESG, safety, and water management.

There are a few non-negotiable capabilities that make this work in practice:

A single, configurable data model across domains. You need a shared foundation for facilities, organizational hierarchies, assets, permits, sources, and activities. Configurability matters because no two organizations structure their operations, risk taxonomies, and reporting boundaries the same way. A platform must adapt to your reality without forcing constant customization projects.

Built-in lineage from ingestion to disclosure. Data lineage must be automatic and subject to queries: source record → transformation → calculation → approval → report output. When an auditor asks, “Where did this number come from?” the response should be a trace, not a manual reconstruction.

Integrated workflows with role-based control. Review and approval steps, exception handling, and corrective actions must be part of the system, with clear segregation of duties. That means the platform captures the process, not just the final number.

Evidence management tied directly to metrics. Supporting documents, lab results, permits, and attestations should be attached to the relevant records, time periods, and workflow steps. Evidence should travel with the data, not live in a separate repository.

Automation where it reduces risk, not just effort. Integrations and automated data capture reduce manual entry errors. Consistent calculations reduce “spreadsheet drift.” Automated validations and controls reduce the chance that bad data reaches disclosure.

Cross-domain reporting with consistent governance. ESG rollups, compliance reports, safety dashboards, and water performance indicators should be generated from the same governed data foundation, ensuring consistency across external disclosures and internal operations.

Where Locus Technologies differentiates configurable, integrated, and audit-first lineage

Many vendors can help you “produce a report,” but can they help you defend that report under audit—across multiple environmental and operational domains?

Locus Technologies develops purpose-built software as a configurable and integrated platform spanning EHS, ESG, Safety, and water management, with the controls and traceability required for audit readiness. The differentiation isn’t a single feature; it’s an architecture and operating model:

Unified platform versus point solutions. Old-school point solutions optimize one domain (e.g. safety incidents or ESG reporting) and then rely on integrations, exports, and manual reconciliation to bridge gaps. That works until an audit tests consistency across domains. Locus Technologies supports cross-functional data governance by design, reducing the risk of mismatched facility lists, inconsistent boundaries, and conflicting numbers.

Configurable workflows and data structures versus rigid templates. Audits test how work actually gets done across your organization: site by site, process by process. A rigid tool forces workarounds and workarounds create audit risk. Locus Technologies’ configurability enables organizations to align the platform to their real operating model: approvals, exceptions, controls, evidence requirements, and reporting boundaries, without turning every change into a custom code project.

Audit-ready lineage as a core outcome, not an add-on. Many stacks attempt to “bolt on” audit trail concepts after the fact. In practice, audit readiness depends on capturing lineage at every step: ingestion, transformation, calculation, and workflow. Locus software is oriented around maintaining traceability, so teams can respond quickly, consistently, and defensibly when scrutiny arrives.

Water management integrated with broader environmental and safety data. Water is often treated as either a compliance niche or a sustainability narrative. In reality, it’s both, and it intersects with operations, risk, and ESG commitments. Managing water alongside EHS, ESG, and safety on one platform improves consistency, accelerates audit response, and supports credible disclosures.

The broader point is simple: audit readiness is an emergent property of an integrated, configurable platform with embedded governance. It cannot be reliably achieved through disconnected tools and after-the-fact documentation.

A practical audit-readiness checklist for environmental data

If you want to pressure-test your current approach, ask yourself:

- Can we reproduce any reported number exactly as it was reported last year, including the factors and boundaries used at the time?

- Can we trace a reported ESG metric to site-level source records, with documented approvals and evidence, without emailing five different people?

- Do we have one authoritative facility and organizational hierarchy shared across EHS, safety, ESG, and water metrics?

- Are exceptions, overrides, and corrections captured with rationale and approvals, or do they live in “side conversations”?

- Can we demonstrate role-based access and segregation of duties in the system of record?

If any of these answers are “not consistently,” you don’t just have a tooling issue. You have an audit exposure issue.

The bottom line: the unified platform is the credibility platform

Organizations are right to invest in EHS performance, safety excellence, and ESG transparency. But the next chapter is about proof. Stakeholders increasingly expect the same rigor for environmental and sustainability data as for financial data.

Audit-ready lineage is the foundation. It reduces risk, accelerates audit response, and strengthens credibility by connecting metrics to reality through a defensible chain of custody. That’s why the strategic choice isn’t simply “Which tool helps us report?” It’s “Which platform helps us govern, connect, and defend our environmental data across EHS, ESG, Safety, and water management?”

A unified, configurable, integrated platform that was built for lineage turns audit readiness from a recurring fire drill into a repeatable capability. And in a world of continuous scrutiny, repeatable capability is what separates organizations that scramble from organizations that lead.

Neno Duplan

Founder & CEO

As Founder and CEO of Locus Technologies, Dr. Duplan spent his career combining his understanding of environmental science with a vision of how to gather, aggregate, organize, and analyze environmental data to help organizations better manage and report their environmental and sustainability footprints. During the 1980’s, while conducting research as a graduate student at Carnegie Mellon, Dr. Duplan developed the first prototype system for an environmental information management database. This discovery eventually lead to the formation of Locus Technologies in 1997.

As technology evolved and new guidelines for environmental stewardship expanded, so has the vision Dr. Duplan has held for Locus. With the company’s deployment of the world’s first commercial Software-as-Service (SaaS) product for environmental information management in 1999 to the Locus Mobile solution in 2014, today Dr. Duplan continues to lead and challenge his team to be the leading provider of cloud-based EH&S and sustainability software.

Dr. Duplan holds a Ph.D. in Civil Engineering from the University of Zagreb, Croatia, an M.S. in Civil Engineering from Carnegie-Mellon, and a B.S. in Civil Engineering from the University of Split, Croatia. He also attended advanced Management Training at Stanford University.

Locus is the only self-funded water, air, soil, biological, energy, and waste EHS software company that is still owned and managed by its founder. The brightest minds in environmental science, embodied carbon, CO2 emissions, refrigerants, and PFAS hang their hats at Locus, and they’ve helped us to become a market leader in EHS software. Every client-facing employee at Locus has an advanced degree in science or professional EHS experience, and they incubate new ideas every day – such as how machine learning, AI, blockchain, and the Internet of Things will up the ante for EHS software, ESG, and sustainability.